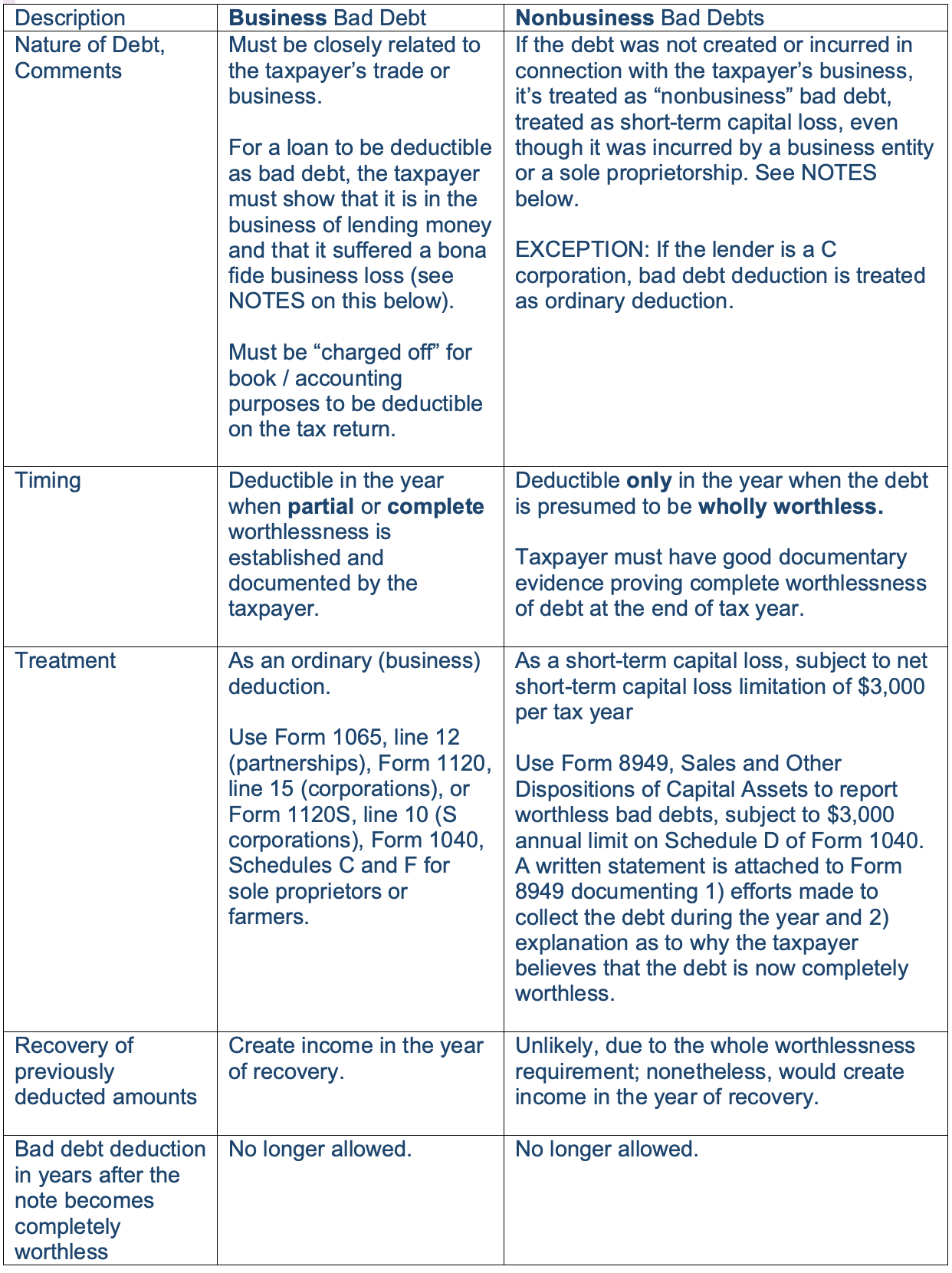

When we lend someone money and stand not to recover the full amount because our lender is unable to pay us (for whatever reason), we would have bad debt that is reflected as such for both accounting and tax purposes.

For most individual taxpayers, the write-off of the unpaid portion of the debt only occurs in the year when complete worthlessness can be clearly demonstrated (i.e., once all attempts to collect money from the borrower have ceased). Moreover, nonbusiness bad debt deductions are treated as short-term capital losses, subject to an annual net short-term capital loss limitation of $3,000.

Qualifying for an ordinary business deduction (as opposed to a short-term capital loss) allowable for business taxpayers either for partial or complete worthlessness of debt is generally tricky for most businesses. The business that intends to take that deduction must demonstrate that lending money is its primary business activity and that its loan to the borrower was one of many loans it had extended in the course of its business of lending money.

To see a profit and loss template for a truck owner-operator business, take a look at this blog post on our site. Profit and Loss Template for a Truck Owner-Operator Business

To see a profit and loss template for a truck owner-operator business, take a look at this blog post on our site

NOTES:

Business of Lending Money

A taxpayer who can establish that he or she is in the trade or business of lending money normally can claim a business bad debt deduction for uncollectible loans. In determining whether the taxpayer is in the trade or business of lending money, the courts generally consider: (1) the total number of loans made; (2) the time period over which the loans were made; (3) the adequacy and nature of the taxpayer’s records; (4) whether the loan activities were kept separate and apart from the taxpayer’s other activities; (5) whether the taxpayer sought out the lending business; and (6) the amount of time and effort expended in the lending activity and the relationship between the taxpayer and his debtors (Henderson, 375 F.2d 36 (5th Cir. 1967); Serot, T.C. Memo. 1994-532, aff’d, 74 F.3d 1227 (3d Cir. 1995)).

See https://www.thetaxadviser.com/issues/2016/mar/deducting-business-bad-debts.html for more detail.

ADDITIONAL RESOURCES:

- https://www.law.cornell.edu/uscode/text/26/166 (IRC Code 166, Bad Debts)

- https://www.irs.gov/taxtopics/tc453 (additional materials from the IRS)