Comparison of Partnership versus S Corporation Tax Structures

At Glasgow Knight Financial, we often receive the question about the difference between partnership and S corporation tax structures and our clients asking to recommend the best structure for their small to medium-sized business. In order to answer this question fully, in addition to the background statutory information, a mathematical illustration should be presented to assist with the choice.

Background Information

• A limited liability company is a creature of state law.

• LLCs with two or more members can choose their form of taxation for Federal income tax purposes.

• The default tax classification is a partnership.

• S corporation and C corporation structures are elective and available at any time.

• Because of the double-taxation regime of C corporations and their shareholders, C corporations are not advised at this time.

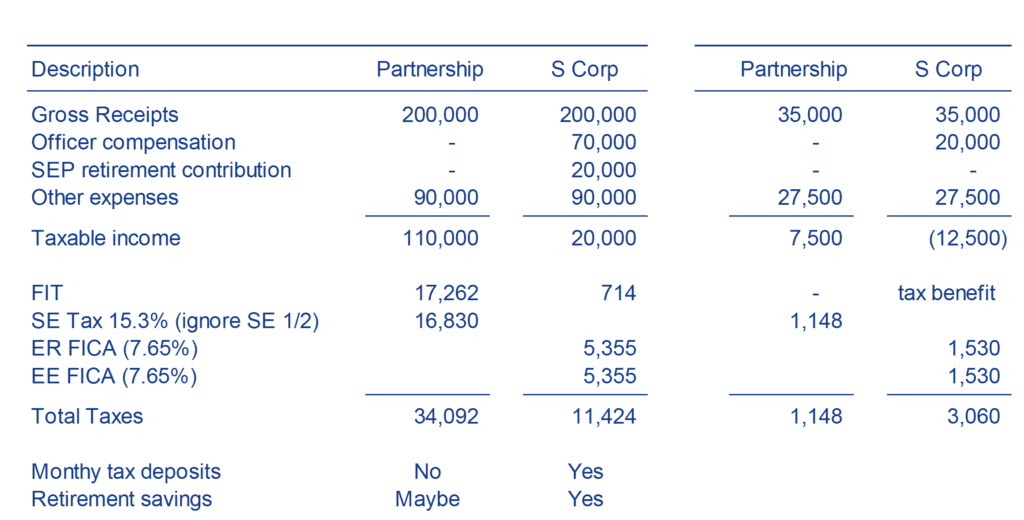

Two Scenarios

• Consider the following two scenarios of a partnership and an S corporation structures with relatively high and relatively low taxable incomes.

• For the sake of simplicity, no allocations have been made for the two 50/50 partners (shareholders) in these two mathematical illustrations. Also note that no adjustment has been made for the 1/2 of the self-employment tax deduction, again to keep the illustration simple:

Notes on the Scenarios

• Distributive shares of partnership income are generally subject to both Federal income tax and self-employment taxes (at a rate of 15.3%).

• Partners in a partnership do not get “paid” wages.

• Distributive shares of S corporation income are not subject to self-employment taxes.

• S corporations are operating under a watchful eye of the IRS empowered by the U.S. Congress to adjust S corporation officer compensation when those amounts do not appear to be reasonable.

Recommendation

• As the two scenarios above illustrate, setting up a limited liability company taxed as a partnership in the earlier years of operation appears to be a prudent step.

• At a certain point, an S corporation election may need to be made. After this election is made, former “partners” would become “officers” and the S corporation would be required to pay reasonable officer compensation subject to Federal income and FICA taxes.

• An added benefit of an S Corporation: it is much easier to set up a Simplified Employee Pension plan in an S corporation than in a partnership. The maximum contribution to SEP plan is 25% of earned income (W-2 wages), limited to $61,000 in 2022.